rizzz your wealth

Save Lakhs with the Ultimate Financial Secret – Renting vs Buying for Maximum Wealth"

At Wealthriz, we reveal how renting and investing in SIPs can help you save lakhs in interest and grow a ₹2.4 crore corpus over 20 years. Unlock the smart financial strategy for true wealth and freedom today.

9/13/20245 min read

Unlock the Secret to Financial Freedom: Why Renting and Investing Can Outperform Home Buying

Many people dream of owning a home, but they often overlook the financial pitfalls of a home loan. While owning a home may seem like the ideal investment, the reality is that home loans tie you down to years of interest payments and financial constraints. Here’s a smarter, more flexible strategy that can build more wealth over time: Rent a Better Home and Invest the Difference in SIPs.

Let’s break it down with data and show why this is a golden financial advice for anyone looking to optimize their finances.

The Home Loan Trap: Why It Can Drain Your Finances

When you take a home loan, the biggest part of your EMI (Equated Monthly Installment) goes toward interest, especially in the initial years. Consider the following example:

Loan Amount: ₹50,00,000

Average Home Loan Interest Rate: 8%

Loan Tenure: 20 years

Monthly EMI: ₹41,822

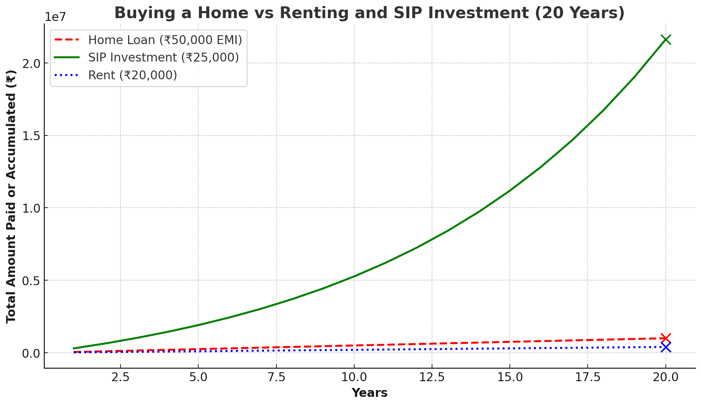

By the end of 20 years, you would have paid ₹1,00,37,280 in total, which includes over ₹50 lakh in interest alone. This is a huge financial burden, and the property’s appreciation may not give you the massive returns you expect, as real estate typically appreciates by only 4-6% annually.

The Smart Alternative: Renting and SIP Investing

Now, imagine instead of buying, you decide to rent a home and invest the difference in a high-return instrument like a Systematic Investment Plan (SIP). Here’s how this strategy can set you up for greater wealth and financial freedom:

1. Rent a Better Home Than You Could Afford to Buy:

When buying a home with a loan, your choice is limited to what you can afford with your EMI. For instance, a ₹50,00,000 loan might get you a 2 BHK flat. However, with renting, you can live in a better, more premium home for less.

Rent Example: You rent a more spacious or better-located home for ₹20,000 a month. That’s less than half of what you would pay in an EMI!

2. Invest the Difference in SIPs:

Instead of paying ₹50,000 every month as an EMI, you pay ₹20,000 in rent and invest ₹25,000 in a SIP with an average annual return of 12%. This smart investment allows you to harness the power of compounding and build significant wealth over time.

Monthly Rent: ₹20,000

SIP Investment: ₹25,000

Leftover Savings: ₹5,000 (which you can either save, invest, or use for other expenses)

The Power of Compounding: How Your SIP Grows Over Time

Example: Investing ₹25,000 Monthly in SIP

Let’s calculate how much your ₹25,000 monthly investment will grow over 20 years with an annual return of 12%, which is a realistic figure based on the historical performance of equity mutual funds:

Investment Tenure: 20 years

Monthly Investment: ₹25,000

Expected Annual Return: 12%

Total Corpus After 20 Years: ₹2.4 crore

That’s ₹2.4 crore without any debt hanging over your head! Meanwhile, if you’d taken a home loan, you’d be left with a house that may have appreciated but might not be as liquid or as flexible as cash.

The Bonus: Flexibility and Extra Savings

Here’s where the magic of this strategy really shines:

Better Living Conditions:

Renting allows you to live in a better house than the one you would have bought. You can upgrade your lifestyle by choosing a location or size that would be unaffordable if you were buying it with a loan. For example, instead of settling for a 2 BHK, you might be able to afford a 3 BHK in a better area, thanks to renting flexibility.Flexibility in Finances:

Even after paying your rent and investing in SIPs, you’ll still have ₹5,000 left from what you would’ve paid as an EMI. This amount can be used for emergencies, more investments, or personal expenses, giving you additional financial security.No Debt Pressure:

By choosing to rent and invest, you’re not locked into a long-term debt. If your income changes, you can adjust your rent or SIP contributions accordingly, giving you more financial flexibility compared to a home loan, which requires you to stick to EMI payments no matter what.

The Math: Buying vs. Renting and SIP Investing

Why Renting and Investing is a Wealth-Building Strategy

Massive Wealth Accumulation:

Over 20 years, your ₹25,000 SIP investment can grow to ₹2.4 crore. This kind of return far outpaces the appreciation of most properties over the same time period.Better Use of Your Money:

Instead of sinking your hard-earned money into paying interest on a home loan, you’re investing in an asset that grows and compounds at a much faster rate.More Control Over Lifestyle:

Renting gives you the flexibility to move to better locations or larger homes as your life circumstances change, without the constraints of home ownership. You’re not tied down to one property or mortgage for decades.Liquidity and Freedom:

While a house is a physical asset, it’s not easily liquidated. Your investments in SIPs, on the other hand, can be accessed easily if you ever need funds, giving you more control over your finances.

Conclusion: The Smart Path to Financial Independence

In summary, by opting to rent and invest in SIPs, you can live in a better home, accumulate massive wealth through compounding, and maintain financial flexibility. This strategy allows you to avoid the debt burden of a home loan, all while building a far greater financial corpus over 20-25 years.

Final Thought: Why This is the Golden Strategy

Renting is often seen as “throwing money away,” but in reality, when paired with disciplined investing, it becomes a powerful wealth-building tool. You’re not only saving on high loan interest but also putting your money to work through compounding returns. Over 20 years, this strategy can leave you with a massive financial cushion, whether you choose to buy a home outright or continue renting.

This is your golden financial secret for securing long-term wealth and freedom

Frequently Asked Questions (FAQs)

Is renting really better than buying a home?

Renting can be better in the short to medium term if you invest the savings smartly. By renting, you avoid massive interest payments on home loans and can invest the difference in high-return investments like SIPs, which compound over time, leading to greater wealth accumulation.

What is a SIP, and why should I invest in it?

A Systematic Investment Plan (SIP) allows you to invest a fixed amount regularly in mutual funds, typically equity funds. Over time, SIPs benefit from compounding and tend to offer higher returns (historically around 12% annually) compared to property appreciation.

How can I live in a better house by renting?

When you take a home loan, you are restricted to a property that fits within your EMI budget. By renting, you can often afford to live in a better home or a more desirable location at a lower monthly cost, which wouldn't be possible with an equivalent EMI.

What happens if the SIP doesn't perform well?

SIP investments, especially in equity mutual funds, are subject to market fluctuations. However, historically, over long periods (10-20 years), the market has averaged around 10-12% returns. Diversifying your SIP investments and reviewing them regularly can help mitigate risks.

Is it safe to rely on renting for the long term?

Renting offers flexibility, and you can always change your decision based on your financial circumstances. In the long term, investing the money you save through renting can build a substantial financial corpus, giving you the option to buy a home later without needing a loan.

What if property prices rise significantly over time?

While property values may increase, they generally appreciate at 4-6% annually, which is often lower than the return on investments like SIPs (which have historically averaged around 10-12% annually). The liquidity and compounding effect of SIPs make them a stronger wealth-building tool.

How do I start with this strategy?

First, calculate your budget: compare potential EMI payments with renting costs. Then, invest the savings in a SIP. It’s essential to stay consistent with your investments and choose funds that align with your long-term goals. Revisit and adjust your investments periodically to ensure you're on track.