rizzz your wealth

How Banks Work: Understanding Money and Credit

Discover how banks manage money and credit, including deposits, loans, and financial services. Learn about banking operations and their crucial role in the economy.

6/11/20249 min read

Introduction

Banks are fundamental institutions in the financial system, playing a vital role in the economy. They provide a safe place for people to save their money, offer loans and credit, and facilitate payments. This blog will explore how banks work, including the mechanisms of money and credit, in a detailed and easily understandable way. We will delve into various aspects such as how banks manage deposits, the process of lending, how they make money, and their role in the economy.

Table of Contents

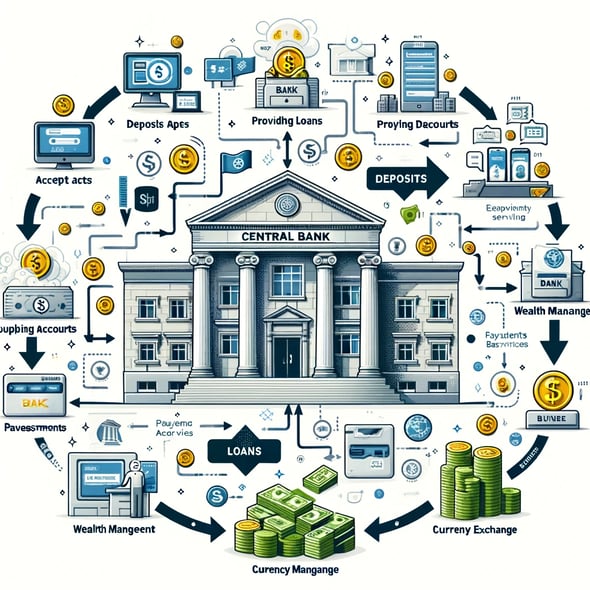

What is a Bank?

How Banks Manage Deposits

The Process of Lending

How Banks Make Money

The Role of Credit

Types of Banks

How Central Banks Influence the Economy

Technological Innovations in Banking

Challenges Faced by Banks

Conclusion

1. What is a Bank?

Definition: A bank is a financial institution licensed to receive deposits and make loans. Banks may also provide financial services such as wealth management, currency exchange, and safe deposit boxes.

Banks serve as intermediaries between depositors, who supply capital, and borrowers, who demand capital. This intermediary function is critical in facilitating economic activity and growth.

Functions of a Bank

Accepting Deposits: Banks accept deposits from the public, providing a safe place to store money. These deposits can be in the form of savings accounts, checking accounts, and fixed deposits.

Providing Loans: Banks provide loans to individuals, businesses, and governments. These loans can be for various purposes, such as buying a house, starting a business, or funding public projects.

Payment and Settlement Services: Banks facilitate payments between parties through various instruments like checks, credit cards, and electronic transfers.

Wealth Management: Banks offer investment and advisory services to help clients manage their wealth.

Currency Exchange: Banks exchange foreign currency for domestic currency and vice versa.

2. How Banks Manage Deposits

When you deposit money in a bank, it doesn't just sit there. Banks use these deposits to make loans and investments, generating returns that allow them to pay interest on deposits and make a profit.

Types of Deposits

Savings Accounts: These accounts pay interest on the deposited funds. They are typically used for short-term savings needs. Savings accounts offer a modest interest rate and high liquidity, allowing customers to withdraw funds anytime.

Checking Accounts: These are used for daily transactions. They offer high liquidity but usually pay little or no interest. Checking accounts often come with check-writing privileges, debit cards, and online bill payment services.

Fixed Deposits (Certificates of Deposit): These are deposits made for a fixed term with a higher interest rate. The funds are not accessible until the end of the term without a penalty. Fixed deposits offer higher interest rates compared to savings and checking accounts, making them suitable for long-term savings.

How Deposits Are Used

Banks use the money deposited by customers to provide loans to other customers. The process works as follows:

Deposit Collection: Banks collect deposits from customers.

Loan Provision: A portion of these deposits is used to provide loans to individuals and businesses.

Interest Earnings: The bank earns interest on the loans provided.

Interest Payments: A part of the interest earned from loans is paid to depositors as interest on their deposits.

This cycle allows banks to generate income while providing services to both depositors and borrowers.

3. The Process of Lending

Banks use the deposits they receive to provide loans to individuals, businesses, and governments. The lending process involves evaluating the creditworthiness of borrowers and setting the terms of the loan.

Types of Loans

Personal Loans: Unsecured loans provided to individuals for personal use, such as education, medical expenses, or vacations. These loans typically have higher interest rates due to the lack of collateral.

Mortgage Loans: Secured loans provided for the purchase of real estate. The property serves as collateral. Mortgage loans usually have lower interest rates and longer repayment periods.

Business Loans: Loans provided to businesses for various purposes, including working capital, expansion, and equipment purchase. These loans can be secured or unsecured, depending on the business's creditworthiness and the loan amount.

The Lending Process

Application: The borrower submits a loan application detailing their financial status and the purpose of the loan.

Credit Evaluation: The bank assesses the borrower’s creditworthiness by reviewing their credit history, income, and existing debts. This evaluation helps the bank determine the risk associated with lending to the borrower.

Approval: If the borrower meets the bank’s criteria, the loan is approved. The bank may also require collateral to secure the loan.

Disbursement: The funds are transferred to the borrower. The disbursement can be a lump sum or in installments, depending on the loan agreement.

Repayment: The borrower repays the loan in installments over an agreed period, including interest. The repayment schedule is usually monthly, and the interest rate can be fixed or variable.

4. How Banks Make Money

Banks make money primarily through the interest spread—the difference between the interest they pay on deposits and the interest they charge on loans. Additionally, they earn from fees and commissions for various services.

Sources of Bank Income

Interest Income: The primary source of income, derived from the interest on loans and investments. Banks lend money at higher interest rates than they pay on deposits, earning a profit from the difference.

Fees and Charges: Banks charge fees for account maintenance, overdrafts, wire transfers, and other services. These fees contribute significantly to the bank's revenue.

Trading and Investments: Banks invest in securities, foreign exchange, and other financial instruments to generate income. Investment banking activities, such as underwriting and mergers and acquisitions, also contribute to income.

Example of Bank Income

Source of IncomePercentage of Total Income

5. The Role of Credit

Credit is the ability to borrow money with the promise to repay it in the future, typically with interest. Credit is essential for economic growth as it enables individuals and businesses to invest in opportunities that they might not be able to afford with their current resources.

Types of Credit

Revolving Credit: This type of credit allows the borrower to use funds up to a limit and repay them as needed, such as credit cards. Revolving credit offers flexibility, as borrowers can use and repay the funds multiple times.

Installment Credit: This involves borrowing a fixed amount and repaying it over time with regular payments, such as car loans and mortgages. Installment credit is suitable for large, one-time purchases that require structured repayment.

Importance of Credit

Credit plays a crucial role in the economy by:

Facilitating Consumption: Credit allows consumers to purchase goods and services they cannot afford upfront, boosting economic activity.

Enabling Investment: Businesses use credit to invest in new projects, equipment, and expansion, driving growth and innovation.

Smoothing Cash Flow: Credit helps individuals and businesses manage cash flow by providing funds when income is insufficient.

6. Types of Banks

There are various types of banks, each serving different functions within the financial system.

Commercial Banks

Commercial banks offer services to the general public and businesses, including accepting deposits, providing loans, and other financial services. They play a vital role in the economy by facilitating daily financial transactions.

Investment Banks

Investment banks specialize in services related to financial markets, such as underwriting, mergers and acquisitions, and trading of securities. They help companies raise capital by issuing stocks and bonds.

Central Banks

Central banks manage a country’s monetary policy and regulate the banking system. Examples include the Federal Reserve in the United States and the European Central Bank. Central banks control the money supply and interest rates to achieve economic stability.

7. How Central Banks Influence the Economy

Central banks use monetary policy tools to influence the economy. They control the money supply and interest rates to achieve economic objectives like controlling inflation, managing employment levels, and ensuring financial stability.

Monetary Policy Tools

Open Market Operations: Buying and selling government securities to influence the money supply. When central banks buy securities, they inject money into the economy, increasing the money supply. When they sell securities, they reduce the money supply.

Interest Rate Adjustments: Changing the benchmark interest rate to influence borrowing and spending. Lowering interest rates makes borrowing cheaper, encouraging spending and investment. Raising interest rates makes borrowing more expensive, reducing spending and controlling inflation.

Reserve Requirements: Setting the minimum reserves each bank must hold to ensure liquidity. By increasing reserve requirements, central banks reduce the money banks can lend, slowing economic activity. Lowering reserve requirements increases the money available for lending, stimulating the economy.

Example of Central Bank Influence

Monetary Policy Tool Effect on Economy

8. Technological Innovations in BankingMy post content

Online and Mobile Banking

Online and mobile banking have revolutionized the banking industry by making financial services more accessible and convenient. Customers can now manage their finances from the comfort of their homes or on the go, eliminating the need to visit a bank branch for routine transactions. These platforms offer a range of services, including checking account balances, transferring funds, paying bills, and applying for loans.

Benefits of Online and Mobile Banking:

Convenience: Customers can perform transactions anytime and anywhere.

Speed: Transactions are processed quickly, often in real-time.

Cost-Effective: Reduces the need for physical branches and staff, lowering operational costs.

Accessibility: Provides access to banking services for people in remote or underserved areas.

Fintech Innovations

Fintech, short for financial technology, refers to the use of technology to provide innovative financial services. Fintech companies are leveraging cutting-edge technologies to offer new products and services that enhance the customer experience and improve efficiency in the financial sector.

Examples of Fintech Innovations:

Peer-to-Peer Lending: Platforms like LendingClub and Prosper connect borrowers with individual lenders, bypassing traditional banks.

Digital Wallets: Services like PayPal, Apple Pay, and Google Wallet allow users to make payments and transfer money digitally.

Blockchain and Cryptocurrencies: Blockchain technology underpins cryptocurrencies like Bitcoin, providing a secure and transparent way to record transactions.

Robo-Advisors: Automated investment platforms like Betterment and Wealthfront use algorithms to provide personalized investment advice and portfolio management.

Artificial Intelligence and Machine Learning

Artificial intelligence (AI) and machine learning (ML) are transforming the banking industry by automating processes, enhancing customer service, and improving risk management. These technologies analyze vast amounts of data to make predictions, detect patterns, and optimize decision-making.

Applications of AI and ML in Banking:

Fraud Detection: AI algorithms analyze transaction data to identify suspicious activities and prevent fraud.

Customer Service: AI-powered chatbots and virtual assistants provide 24/7 customer support, answering queries and assisting with transactions.

Personalized Financial Advice: AI analyzes customer data to offer tailored financial advice and product recommendations.

Credit Scoring: Machine learning models assess credit risk by analyzing a broader set of data points compared to traditional methods.

Challenges Faced by Banks

Despite the numerous benefits of technological advancements, banks face several challenges in today’s rapidly evolving financial landscape.

Regulatory Compliance

Banks operate in a highly regulated environment to ensure the stability and security of the financial system. Compliance with these regulations can be complex and costly, requiring banks to invest in robust compliance programs and systems. Regulatory requirements vary across different jurisdictions, adding to the complexity for banks operating internationally.

Key Areas of Regulation:

Anti-Money Laundering (AML): Banks must implement measures to detect and prevent money laundering activities.

Know Your Customer (KYC): Banks are required to verify the identity of their customers to prevent fraud and financial crimes.

Data Protection: Regulations like the General Data Protection Regulation (GDPR) in Europe mandate strict data privacy and protection measures.

Cybersecurity Threats

With the increasing reliance on digital banking, banks are more vulnerable to cyber-attacks. Cybersecurity threats can result in significant financial losses, reputational damage, and legal liabilities. Banks must continually invest in advanced security measures to protect their systems and customer data from cybercriminals.

Common Cybersecurity Threats:

Phishing Attacks: Cybercriminals trick individuals into providing sensitive information through deceptive emails or websites.

Malware: Malicious software is used to gain unauthorized access to banking systems and data.

Ransomware: Attackers encrypt a bank's data and demand a ransom for its release.

Data Breaches: Unauthorized access to sensitive customer data, resulting in data loss and potential identity theft.

Economic Uncertainty

Economic conditions can significantly impact the banking industry. Factors such as interest rate fluctuations, inflation, and economic downturns affect banks' profitability and stability. During economic uncertainty, banks may face increased loan defaults and reduced demand for financial products and services.

Economic Challenges:

Interest Rate Risk: Changes in interest rates can affect banks' net interest margins and profitability.

Credit Risk: Economic downturns can lead to higher default rates on loans, impacting banks' asset quality.

Market Risk: Volatility in financial markets can affect the value of banks' investments and trading portfolios.

Conclusion

Banks are essential institutions that manage money, provide credit, and facilitate economic growth. Understanding how banks work, from managing deposits and lending to leveraging technology, provides insight into their essential role in the economy. Despite the challenges they face, banks continue to adapt and innovate, ensuring they remain integral to our financial system.

"Banks play a pivotal role in the financial system, acting as intermediaries that facilitate economic activity and growth by managing deposits, providing loans, and ensuring financial stability."

FAQs

1. What is a bank?

Answer: A bank is a financial institution licensed to receive deposits, make loans, and provide various financial services such as wealth management, currency exchange, and safe deposit boxes.

2. How do banks manage deposits?

Answer: Banks manage deposits by using them to make loans and investments, generating returns that allow them to pay interest on deposits and make a profit.

3. What are the types of loans banks provide?

Answer: Banks provide various types of loans, including personal loans, mortgage loans, and business loans, each serving different financial needs.

4. How do banks make money?

Answer: Banks make money primarily through the interest spread—the difference between the interest they pay on deposits and the interest they charge on loans. They also earn from fees and commissions for various services.

5. What is the role of credit in the economy?

Answer: Credit enables individuals and businesses to invest in opportunities that they might not be able to afford with their current resources, driving economic growth and development.

Banks: The Hidden Architects of Wealth and Credit in Our Economy